A CPA-attorney is a licensed professional who holds both a Juris Doctor degree and an active Certified Public Accountant designation, and who applies both credentials simultaneously within a single client engagement.

Most estate plans in Massachusetts and Maine are prepared by two separate professionals: an attorney who drafts the legal documents and a CPA who models the tax outcomes.

The CPA-attorney collapses both roles into a single engagement — so the legal structure and the tax outcome are designed together, not reconciled after the documents are signed.

Key Takeaways

- A CPA-attorney designs the legal structure and models the tax outcome in the same engagement — eliminating the handoff gap between two separate professionals that standard estate plans rely on.

- Massachusetts imposes a state estate tax above $2,000,000 under M.G.L. c. 65C that applies to the entire estate and is not portable between spouses — making Credit Shelter Trust funding formula accuracy a direct dollar-value planning decision, not a legal formality.

- Maine adds a one-year gift lookback under 36 M.R.S. § 4102 that pulls annual exclusion gifts made within twelve months of death back into the Maine taxable estate — a planning factor most standard estate plan reviews miss entirely.

- A hypothetical Westborough, Massachusetts couple with a $3,400,000 estate saves approximately $120,000 in Massachusetts estate tax through Credit Shelter Trust planning — a saving only achievable when the attorney drafting the trust also runs the tax model before the first document is written.

Schedule a free consultation with Daintria W. McClure, J.D., CPA, to discuss your Massachusetts or Maine estate plan.

What Does a CPA-Attorney Do That a Standard Estate Planning Attorney Cannot?

A standard estate planning attorney designs the legal architecture of an estate plan: the will, the revocable trust, the durable power of attorney, and the healthcare directive.

Tax analysis — modeling how those documents interact with estate tax thresholds, income tax basis, gift tax consequences, and retirement account distribution rules — gets routed to a separate CPA working on a different timeline with incomplete visibility into drafting decisions already made.

A change in trust structure that reduces Massachusetts estate tax exposure may trigger unintended federal income tax consequences that the drafting attorney does not catch until after execution.

Daintria W. McClure, J.D., CPA, runs both analyses before the first draft is written. McClure holds active bar admissions in Massachusetts, Maine, and Florida; admission to practice before the United States Tax Court; and an active CPA designation under the standards of the American Institute of Certified Public Accountants.

Every trust funding formula, beneficiary designation, and ownership structure reflects the actual tax consequence for that family’s specific asset profile — before any document is drafted.

How the CPA Credential Changes Massachusetts Estate Tax Planning

Massachusetts imposes a state estate tax under M.G.L. c. 65C on the estates of decedents dying on or after January 1, 2023, with a gross estate exceeding $2,000,000. The Massachusetts Department of Revenue confirmed on Mass.gov that the Massachusetts estate tax applies to the entire estate, not only the amount above $2,000,000.

A $99,600 credit under M.G.L. c. 65C, § 2A(f) eliminates the tax for estates at or below $2,000,000 and reduces it for larger estates. The Massachusetts estate tax is not portable between spouses — each decedent receives one $99,600 credit, and an unstructured plan wastes that credit permanently at the first death.

The Massachusetts Portability Gap and the Credit Shelter Trust

Federal portability allows a surviving spouse to claim the deceased spouse’s Deceased Spousal Unused Exclusion (DSUE) by filing a timely Form 706 with the IRS within nine months of the first death, with an automatic six-month extension available by filing Form 4768. Massachusetts provides no equivalent portability mechanism.

A Massachusetts estate plan that does not capture the first spouse’s $99,600 credit forfeits that credit permanently, and the surviving spouse’s estate pays Massachusetts estate tax on assets the first spouse’s credit would have sheltered.

A Credit Shelter Trust — also called a Bypass Trust or B Trust — funds up to $2,000,000 into an irrevocable trust at the first death, preserving the first spouse’s $99,600 credit and permanently removing $2,000,000 from the survivor’s taxable Massachusetts estate.

Whether that planning decision is captured or permanently forfeited depends entirely on whether the attorney modeled the Massachusetts estate tax calculation before drafting. Daintria W. McClure, J.D., CPA, calculates projected Massachusetts estate tax liability under both scenarios before drafting a single document — so every trust funding formula reflects the actual tax outcome, not a generic legal template.

The Income Tax Basis Interaction

A Credit Shelter Trust that captures the Massachusetts estate tax credit may sacrifice the federal income tax step-up in basis under IRC § 1014 for appreciated assets that would otherwise pass through the survivor’s taxable estate.

Assets held inside a Credit Shelter Trust do not receive a second IRC § 1014 basis step-up at the survivor’s death. For a Massachusetts family holding a primary residence purchased at $300,000, now worth $900,000, the capital gains tax cost of losing that $600,000 basis step-up can exceed the Massachusetts estate tax savings the trust was designed to produce.

One important carve-out: retirement accounts do not receive an IRC § 1014 step-up under any structure — retirement account distributions are treated as income in respect of a decedent (IRD) under IRC § 691, regardless of whether assets pass through a Credit Shelter Trust or are transferred outright to the survivor.

Daintria W. McClure, J.D., CPA, models the specific dollar values — projected capital gains tax on appreciated assets versus Massachusetts estate tax savings — and builds the trust funding formula around the actual outcome for that family’s balance sheet. A Juris Doctor degree alone does not produce that analysis.

Take Control of Tomorrow by Acting Today

Schedule your consultation with Spinnaker Probate Group and gain peace of mind for the future.

How the CPA Credential Changes Maine Estate Tax Planning

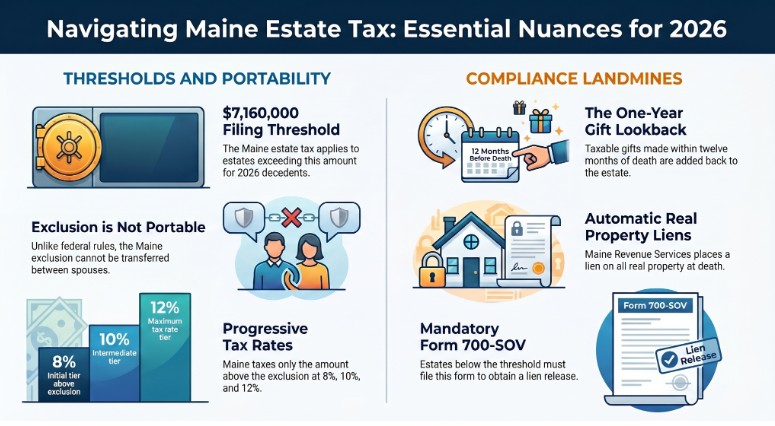

Maine imposes a state estate tax under 36 M.R.S. Chapter 577, administered by Maine Revenue Services, on estates exceeding $7,160,000 for decedents dying in 2026.

Maine taxes only the amount above the exclusion at rates of 8%, 10%, and 12% — unlike Massachusetts, which applies the tax to the entire estate. The Maine estate tax exclusion is not portable between spouses.

Maine adds a planning layer Massachusetts does not impose: the one-year gift lookback. The Maine taxable estate equals the federal taxable estate plus taxable gifts made during the one-year period ending on the date of the decedent’s death under 36 M.R.S. § 4102.

Annual exclusion gifts of $19,000 per recipient that carry no federal gift tax consequence are pulled back into the Maine taxable estate when made within twelve months of death — potentially subject to Maine estate tax at 8% to 12%.

An attorney drafting a lifetime gifting strategy for a Maine client without modeling the one-year lookback date builds a predictable and avoidable tax leak into the plan.

Maine Revenue Services also places an automatic lien on all real and tangible personal property at the time of death.

A Certificate of Discharge of Estate Tax Lien — signed by the Maine State Tax Assessor and recorded at the county Registry of Deeds — is required before any property transfer closes.

Estates below the $7,160,000 threshold must file Form 700-SOV to obtain a lien release. Missing the lien discharge step delays every real property transfer until the filing gap is corrected.

What Federal Portability Planning Looks Like When One Professional Runs Both Sides

For a married couple in Massachusetts or Maine whose combined estate falls below the federal basic exclusion of $15,000,000 per individual — confirmed by the IRS following enactment of the One Big Beautiful Bill Act, signed July 4, 2025 — no federal estate tax applies at either death. Federal portability still matters.

A surviving spouse who does not file a timely Form 706 at the first death risks forfeiting the deceased spouse’s unused federal exclusion.

The IRS confirmed that for estates with no independent filing requirement, Revenue Procedure 2022-32 provides a simplified method to make a late portability election — by filing on or before the fifth anniversary of the decedent’s date of death, with no user fee.

That five-year window exists, but it is a remedial procedure — not a planning strategy. Daintria W. McClure, J.D., CPA, files the Form 706 portability-only return as a standard component of estate administration at the first death, so the DSUE election is preserved without relying on late-relief procedures that require additional filings and carry execution risk.

Take Control of Tomorrow by Acting Today

Schedule your consultation with Spinnaker Probate Group and gain peace of mind for the future.

A Hypothetical: The Westborough, MA Family with a $3.4 Million Estate

Consider a hypothetical married couple in Westborough, Massachusetts. Combined estate: $3,400,000. Assets: primary residence ($1,100,000), investment accounts ($1,500,000), retirement accounts ($600,000), and life insurance payable to the estate ($200,000).

Note: the retirement accounts carry income in respect of a decedent (IRD) treatment under IRC § 691 and do not receive an IRC § 1014 basis step-up under any structure. Life insurance payable to the estate is includable in the Massachusetts gross estate. No estate plan in place.

Without CPA-attorney planning:

The first spouse dies, leaving the full $3,400,000 outright to the surviving spouse. The survivor holds $3,400,000. Using the official Massachusetts DOR rate table under M.G.L. c. 65C — applied to the entire estate — and subtracting the one available $99,600 credit, the Massachusetts estate tax at the survivor’s death is approximately $120,000.

The first spouse’s $99,600 credit was never captured. The $120,000 liability is permanent without restructuring.

With CPA-attorney planning at Spinnaker Probate Group:

A Credit Shelter Trust funds $2,000,000 at the first death — capturing the first spouse’s $99,600 credit and permanently removing $2,000,000 from the surviving spouse’s taxable Massachusetts estate.

The surviving spouse holds $1,400,000 outright — below the $2,000,000 threshold in Massachusetts. Massachusetts estate tax at the survivor’s death: $0. Massachusetts estate tax saved: approximately $120,000.

A timely Form 706 is filed at the first death to preserve federal portability for the $15,000,000 federal basic exclusion under IRC § 2010(c)(3).

The trust funding formula, retirement account beneficiary structure, life insurance ownership analysis, and IRC § 1014 basis planning for the residence are all built into the same document package — because the same professional who drafted the Credit Shelter Trust also ran the Massachusetts estate tax model and the federal capital gains analysis before the first document was written.

That is what a CPA-attorney does differently.

Frequently Asked Questions

What is a CPA-attorney?

A CPA-attorney is a licensed professional who holds both an active Juris Doctor law degree and an active Certified Public Accountant designation, applying both credentials within a single estate planning engagement — drafting legal documents and performing tax analysis without routing work to a separate accounting professional.

Why does a Massachusetts estate plan need both legal and tax analysis in the same engagement?

Massachusetts imposes a state estate tax above $2,000,000 under M.G.L. c. 65C, which is not portable between spouses. Credit Shelter Trust funding formulas determine whether a married couple captures or permanently forfeits the first spouse’s $99,600 credit under M.G.L. c. 65C, § 2A(f) — a calculation requiring CPA-level tax modeling applied to a specific family balance sheet before documents are drafted.

What is the Massachusetts estate tax threshold in 2026, and how does it work?

Massachusetts imposes a state estate tax on estates exceeding $2,000,000 under M.G.L. c. 65C, applying the tax to the entire estate — confirmed by the Massachusetts Department of Revenue on Mass.gov. A $99,600 credit under M.G.L. c. 65C, § 2A(f) eliminates the tax for estates at or below $2,000,000 and reduces it for larger estates. The Massachusetts estate tax is not portable between spouses.

What is the Maine estate tax threshold in 2026?

Maine Revenue Services confirmed the 2026 Maine estate tax exclusion amount is $7,160,000 — up from $7,000,000 in 2025. Maine taxes only the amount above the exclusion at rates of 8% to 12% under 36 M.R.S. Chapter 577. Maine’s one-year gift lookback under 36 M.R.S. § 4102 pulls taxable gifts made within the year of death back into the Maine taxable estate — a factor Maine estate plans must address during the drafting stage.

What is federal portability, and why does it matter for Massachusetts and Maine families?

Federal portability allows a surviving spouse to claim the deceased spouse’s Deceased Spousal Unused Exclusion (DSUE) by filing a timely Form 706 within nine months of the first death. The 2026 federal basic exclusion is $15,000,000 per individual under IRC § 2010(c)(3). For estates with no independent filing requirement that miss the deadline, Revenue Procedure 2022-32 provides a late portability election window of up to five years from the date of death — but filing timely eliminates that remedial risk entirely.

Does a CPA-attorney charge more than a standard estate planning attorney?

Spinnaker Probate Group offers fixed-fee structures for most estate planning engagements. Clients who retain a CPA-attorney avoid the separate CPA engagement required to model tax scenarios — reducing total professional fees while increasing analytical depth. A plan built without tax modeling results in Massachusetts or Maine estate tax exposure that costs multiples of the fee saved by separating the two functions.

What is the IRD rule, and why does it affect retirement account planning?

Income in respect of a decedent (IRD) is income a decedent earned but did not receive before death, governed by IRC § 691. Retirement account balances — including IRAs and 401(k)s — carry IRD treatment and do not receive a federal income tax basis step-up under IRC § 1014 regardless of how the estate is structured. A CPA-attorney accounts for IRD exposure when modeling the total tax cost of a Massachusetts or Maine estate plan, so retirement account beneficiary designations reflect both estate tax and income tax outcomes simultaneously.

Contact Spinnaker Probate Group to schedule a free consultation with Daintria W. McClure, J.D., CPA, and receive a fixed-fee estimate for your Massachusetts or Maine estate plan.