For many Massachusetts and Maine families, probate means months of delays, costly legal fees, and personal family matters made public.

A living trust offers a smarter solution — one that keeps your legacy private, streamlines asset transfers, and reduces stress for loved ones during an already difficult time.

Without it, heirs may face disputes, tax complications, and unnecessary expenses that erode the wealth you worked so hard to build.

At Spinnaker Probate Group, we create customized living trusts that safeguard your assets, honor your wishes, and give your family the gift of peace of mind.

What Does a Living Trust Do for Massachusetts & Maine Families?

A living trust is a legal tool created during your lifetime that holds and manages your assets for your benefit and for the benefit of your heirs.

Unlike a will, a living trust allows property to pass directly to beneficiaries without going through probate — thereby avoiding court delays, public filings, and costly legal fees.

For families in Massachusetts and Maine, this can mean faster access to assets, greater privacy, and reduced emotional strain during an already challenging time.

Key Benefit

The most significant advantage of a living trust is that assets bypass the probate court. Probate can last months or years in Massachusetts and Maine, while a trust ensures beneficiaries receive their inheritance quickly and privately.

Flexibility

Living trusts are fully revocable during your lifetime. You can update beneficiaries, add or remove property, or even dissolve the trust as circumstances change.

Privacy

Unlike wills, which become public record in probate, trust administration remains confidential. This keeps your financial affairs and family decisions private.

Even with a well-drafted trust, missed funding or edge-case assets can still trigger limited court interaction; the goal is to minimize—not merely shift—administration burdens.

Massachusetts vs. Maine at a Glance

- Probate shortcuts: MA offers Voluntary Administration for small estates (≤ $25,000 personal property, excluding 1 vehicle). ME allows a Small-Estate Affidavit after 30 days (cap set by statute and inflation).

- Estate tax filing thresholds: MA effectively eliminates tax at ≤ $2M via credit (for decedents 1/1/2023+). ME’s exclusion is $7,000,000 for 2025 (indexed).

- Real-property TOD deeds: Not allowed in MA; authorized in ME (Uniform Real Property TOD Act).

- Medicaid names: MA MassHealth; ME MaineCare.

Why it matters: these differences shape whether you lean on a trust alone, pair it with deed strategies (ME), or plan around small-estate routes (both states).

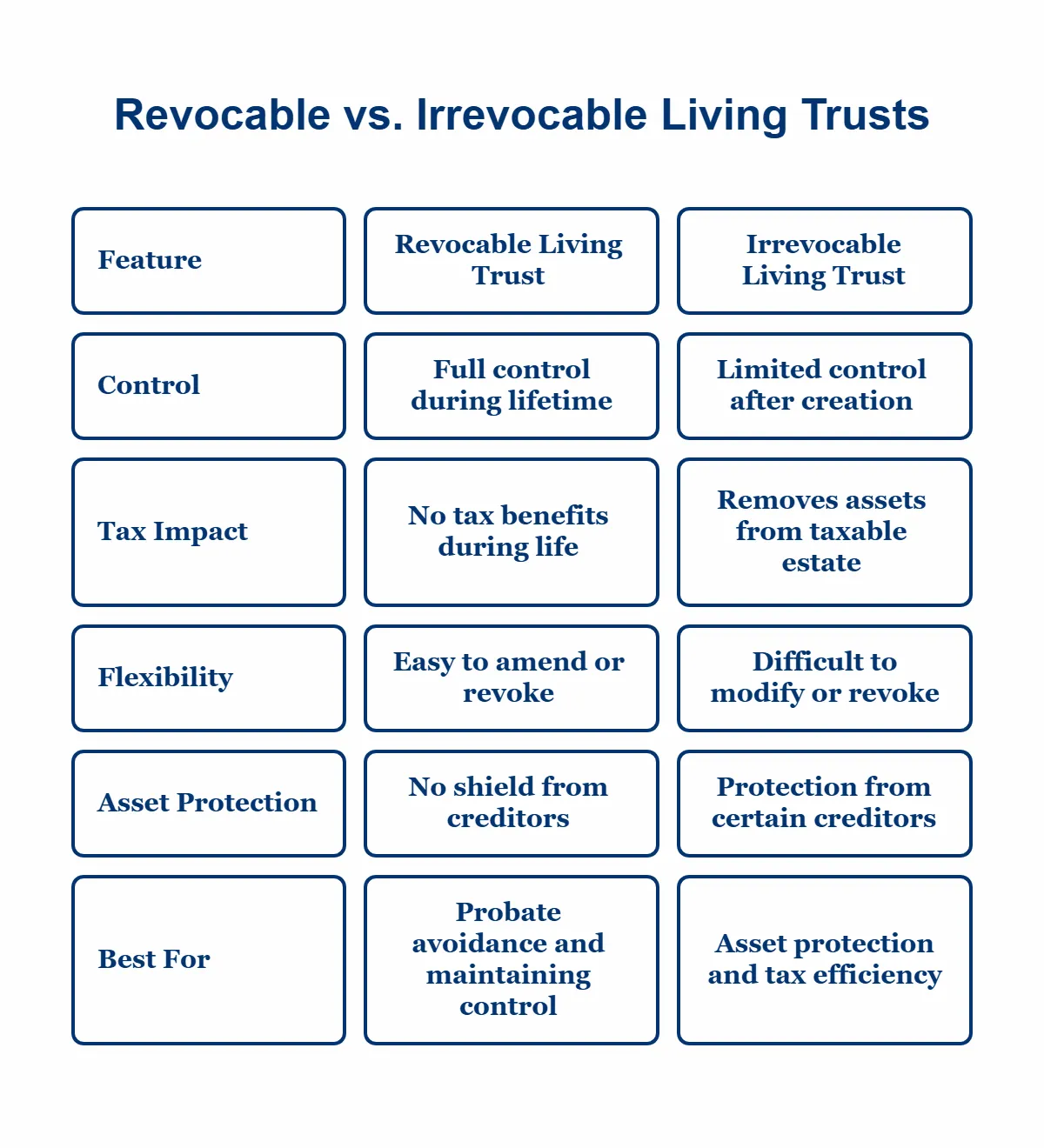

Revocable vs. Irrevocable Living Trusts

Not all living trusts are the same. Choosing between a revocable and an irrevocable trust depends on your goals — whether it is avoiding probate, protecting assets, or achieving tax efficiency.

Feature | Revocable Living Trusts | Irrevocable Living Trusts |

Control | Full control during your lifetime | Limited control once created; assets managed under fixed terms |

Tax Impact | No tax benefits during life; assets remain in taxable estate | May remove assets from taxable estate; potential tax benefits |

Flexibility | Easy to amend or revoke as circumstances change | Difficult to modify or revoke without court approval |

Asset Protection | Does not shield assets from creditors or care costs | May provide protection from certain creditors and long-term care expenses |

Best For | Families seeking probate avoidance and privacy while keeping control | High-net-worth families seeking asset protection and tax efficiency |

Medicaid (MassHealth/MaineCare) Reality Check

- Revocable trusts don’t shield assets for long-term care eligibility; assets are still considered available.

- Irrevocable strategies may provide protection only if completed outside the 5-year look-back and structured correctly.

This is a core reason some families layer a revocable trust for probate avoidance with separate irrevocable planning for care costs. Mass.gov

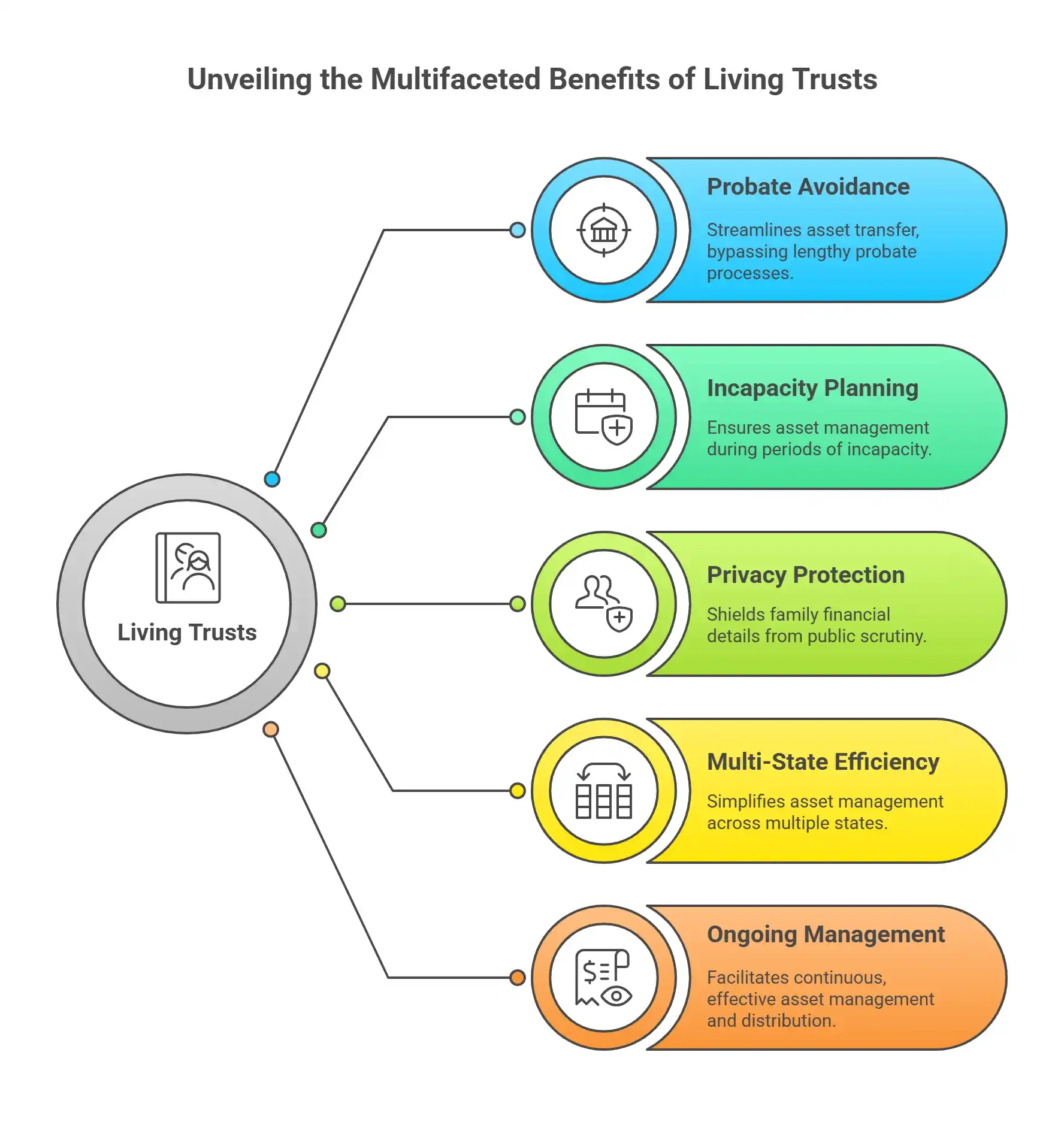

Benefits of Living Trusts for Massachusetts & Maine Families

A living trust is more than a legal document — it’s a tool that brings peace of mind to families.

By avoiding probate, protecting privacy, and ensuring continuity of management, a living trust ensures that your assets are handled smoothly and securely, regardless of what life brings.

Probate Avoidance

The most significant benefit of a living trust is bypassing probate court. Your heirs receive assets faster, privately, and without costly court involvement — sparing them months or even years of delay.

Incapacity Planning

If you become incapacitated, a living trust allows your chosen trustee to step in seamlessly. This avoids the need for court-appointed guardianship and ensures your affairs are managed with dignity and efficiency.

Privacy Protection

Unlike wills, which become public record during probate, living trusts keep family finances and decisions confidential. Sensitive matters remain private and shielded from public scrutiny.

Real Property: MA vs. ME Deed Strategy

- Massachusetts: No transfer-on-death (TOD) deeds; trusts, joint ownership, and lifetime conveyancing are used to avoid probate.

- Maine: TOD deeds are authorized and can keep a home out of probate when used correctly—often paired with a trust for overall coordination.

Multi-State Efficiency

If you own property in more than one state, a living trust eliminates the need for multiple probate proceedings. One trust manages everything, saving time, legal fees, and administrative headaches.

Ongoing Management

Living trusts allow for professional trustee services if desired. This ensures the experienced management of investments, real estate, and business interests, thereby reducing the family’s burden while preserving wealth.

State Estate Tax: What MA & ME Families Should Know

- Massachusetts: A law change effective for decedents dying on or after January 1, 2023, applies a credit that eliminates estate tax for estates ≤ $2,000,000 and reduces tax above that level. Trusts do not remove assets from the taxable estate that are held in a revocable trust.

- Maine: The 2025 exclusion is $7,000,000, indexed for inflation. As with MA, assets in a revocable trust are included in the taxable estate. maine.gov

Translation: probate avoidance ≠ estate-tax avoidance.

We design plans that coordinate trusts, titling, and tax thresholds in your state.

Living Trust Funding Process

Creating trust is step one. Step two—funding—moves assets under the trust’s umbrella so the plan actually functions when needed. We oversee deeds, retitling, and beneficiary alignments.

Real Estate

Homes, vacation properties, and rental units must be retitled with new deeds transferring ownership into the trust’s name. This prevents them from going through probate.

In MA (no TOD), retitling deeds into the trust is critical; in ME, consider whether a TOD deed or trust deed—or both—best fits the family plan. Record promptly and confirm legal descriptions.

Financial Accounts

Bank and investment accounts need to be retitled in the trust’s name. This includes checking, savings, brokerage, and certain retirement accounts, ensuring smooth management and distribution of funds.

Only retitle non-retirement accounts to the trust. For 401(k)/IRA accounts, you typically do not retitle; instead, use beneficiary designations aligned with the plan (primary/contingent, per stirpes where applicable).

Personal Property

Valuable personal items, such as jewelry, artwork, or collectibles, can be transferred using assignment documents. This ensures they are legally recognized as part of the trust.

Business Interests

Business ownership stakes, including LLC shares, partnerships, or corporate stock, can be assigned or retitled into the trust, protecting continuity and avoiding succession disputes.

Insurance Policies

Life insurance and certain financial products may not be owned by the trust, but should list the trust as a primary or contingent beneficiary. This ensures proceeds flow into the trust for management and distribution.

Trustee Selection & Governance (What the Best Plans Do)

- Who should serve: spouse/child vs. corporate trustee (neutrality, continuity, investment platform).

- Successor triggers: incapacity certification standard, death, or resignation.

- Fiduciary duties: prudent investing, record-keeping, accounting, and impartiality among beneficiaries.

- Annual tune-ups: major life events (such as marriage/divorce, sale of home, or business changes), new accounts, or tax-law shifts—all prompt updates.

Common Misconceptions About Living Trusts

Many families hesitate to create a living trust because of myths and misunderstandings. In reality, trusts are practical tools that benefit a wide range of people — not just the wealthy. Here are some of the most common misconceptions we address:

“Trusts are only for the wealthy.”

False. While high-net-worth families often utilize trusts, they are equally beneficial for most homeowners. A living trust ensures that your home and other assets pass smoothly to your heirs without the delays and costs associated with probate.

“I lose control of my assets.”

False — at least for revocable trusts. With a revocable living trust, you maintain full control during your lifetime. You can buy, sell, or transfer property as usual, and you can amend or revoke the trust at any time.

“Trusts eliminate all taxes.”

False. A living trust does not exempt you from income or estate taxes. However, certain types of irrevocable trusts may reduce estate taxes for high-value estates. For most families, the primary benefits are avoiding probate and maintaining privacy.

“One trust document is enough.”

False. Creating trust is only the first step. It must be properly funded by transferring ownership of your assets into the trust. Ongoing updates and maintenance are essential to keep it effective.

Costs vs. Benefits of a Living Trust

Families often wonder whether the cost of setting up a living trust is worthwhile. In nearly all cases, the long-term savings — financial and emotional — far outweigh the initial expense.

Setup Costs

A typical living trust costs between $3,700 and $5,700 to establish, depending on its complexity and the attorney’s experience.

Probate Savings

Probate fees in Massachusetts and Maine often range from $6,500 to $15,000 or more. By avoiding probate, a living trust often pays for itself many times over.

Time Savings

Probate can take anywhere from months to years. A trust allows assets to transfer immediately, sparing loved ones from delays during a difficult time.

Privacy Value

For many families, privacy is priceless. Unlike probate, which is a public process, trust administration remains confidential — shielding your finances and family decisions from public record.

When a Living Trust Isn’t Enough

- Unfunded assets (house still in your name)

- Conflicting beneficiary forms on retirement/insurance

- Creditor/long-term care exposure (revocable trusts don’t protect)

- Multi-state holdings (ancillary probate risk if not captured)

- Old irrevocable trusts needing modernization (e.g., decanting or restatement)

We identify these gaps in a planning session and map the clean-up.

Why Choose Spinnaker Probate Group for Living Trusts?

A living trust isn’t just a legal document — it’s a plan for peace of mind. At Spinnaker Probate Group, we help families in Massachusetts and Maine create trusts that protect assets, simplify transfers, and provide privacy for generations.

Local Knowledge, Tailored Solutions

We understand the unique probate, tax, and property rules in Massachusetts and Maine. Our trust plans are customized to match your family’s goals and state requirements.

Clear, Compassionate Guidance

Many people worry that trusts are too complicated or only for the wealthy. We explain every step in plain language so you feel confident and supported throughout the process.

Cost-Effective Planning

By investing in a living trust now, you save your family thousands in probate fees and months of delay later. We focus on value, not just documents.

Comprehensive Services

From drafting and funding the trust to ongoing updates, our team provides full-service support. You’ll never be left wondering if your trust is complete or effective.

Take control of your legacy. Schedule a consultation with Spinnaker Probate Group now and put the power of a living trust to work for your family.