Without a plan, loved ones may be left facing uncertainty, conflict, or financial strain at the very moment they need comfort and stability.

For families across Massachusetts and Maine, a comprehensive estate plan means children are cared for, spouses are supported, and legacies are preserved without unnecessary court battles or delays.

At Spinnaker Probate Group, we approach estate planning with compassion and clarity, helping you build a future where your family is secure, your wishes are honored, and your love endures long after you’re gone.

Compliance We Follow (MA & ME)

Massachusetts Uniform Trust Code (M.G.L. c. 203E) • Massachusetts Uniform Probate Code (M.G. L. c. 190B) • Maine Uniform Trust Code (MRS Title 18-B) • Maine Uniform Probate Code (MRS Title 18-C).

What Does Estate Planning Mean for Massachusetts & Maine Families?

Estate planning is the process of creating legal strategies to manage how assets are distributed, minimize taxes, and protect loved ones after death or incapacity.

The ultimate goal is to ensure your wishes are honored while minimizing costs, delays, and family stress.

Estate planning combines legal, financial, and personal decisions into one structured plan.

It ensures property transfers smoothly, guardianship for children is clear, and future medical preferences are respected.

Goal

The primary goal is peace of mind. Estate planning eliminates uncertainty by ensuring your instructions are legally binding. It also helps reduce probate delays, court involvement, and unnecessary taxes.

Timeline

Experts recommend reviewing your estate plan every 3–5 years or after major life events, such as marriage, divorce, the birth of a child, or significant financial changes. Keeping documents current ensures they reflect your most recent wishes.

Essential Estate Planning Documents

Every strong estate plan relies on a set of key legal documents that work together to protect you and your family. Each has a distinct purpose in safeguarding wealth, health, and legacy.

Document | Purpose | Key Benefits |

Will | Directs how assets are distributed and names guardians for minor children | Ensures wishes are honored, avoids state intestacy rules that may conflict with your intentions |

Power of Attorney | Grants a trusted person authority to make financial and legal decisions if you become incapacitated | Maintains continuity of bill payments, property management, and legal obligations |

Healthcare Directive | Outlines medical treatment preferences if you cannot speak for yourself | Provides guidance to doctors, prevents family conflict, and ensures your healthcare wishes are clear |

HIPAA Authorization | Authorizes chosen representatives to access medical records | Allows family to make informed medical decisions without privacy law barriers |

Trust Documents | An unfunded revocable trust still forces assets through probate. We provide a personalized funding checklist (including accounts, deeds, and beneficiary designations) and assist you in completing it. | Avoids probate, minimizes taxes, provides privacy, protects beneficiaries, preserves family wealth |

Will

A will determines who inherits your assets and allows you to name guardians for minor children. Without one, state intestacy laws dictate distribution, which may not reflect your wishes.

Power of Attorney

This document authorizes a trusted person to make financial and legal decisions on your behalf if you become incapacitated. It ensures continuity of bill payments, property management, and financial obligations.

Healthcare Directive

Also known as a living will, this document outlines your preferences for medical treatment when you are unable to communicate them yourself. It provides guidance to doctors and peace of mind to loved ones.

HIPAA Authorization

HIPAA authorization ensures that your chosen representatives can access your medical information. Without it, even close family members may face barriers when making urgent healthcare decisions.

Trust Documents

Trusts are powerful tools for asset protection. They can avoid probate, minimize taxes, provide privacy, and secure financial stability for future generations. Options include revocable, irrevocable, special needs, and charitable trusts.

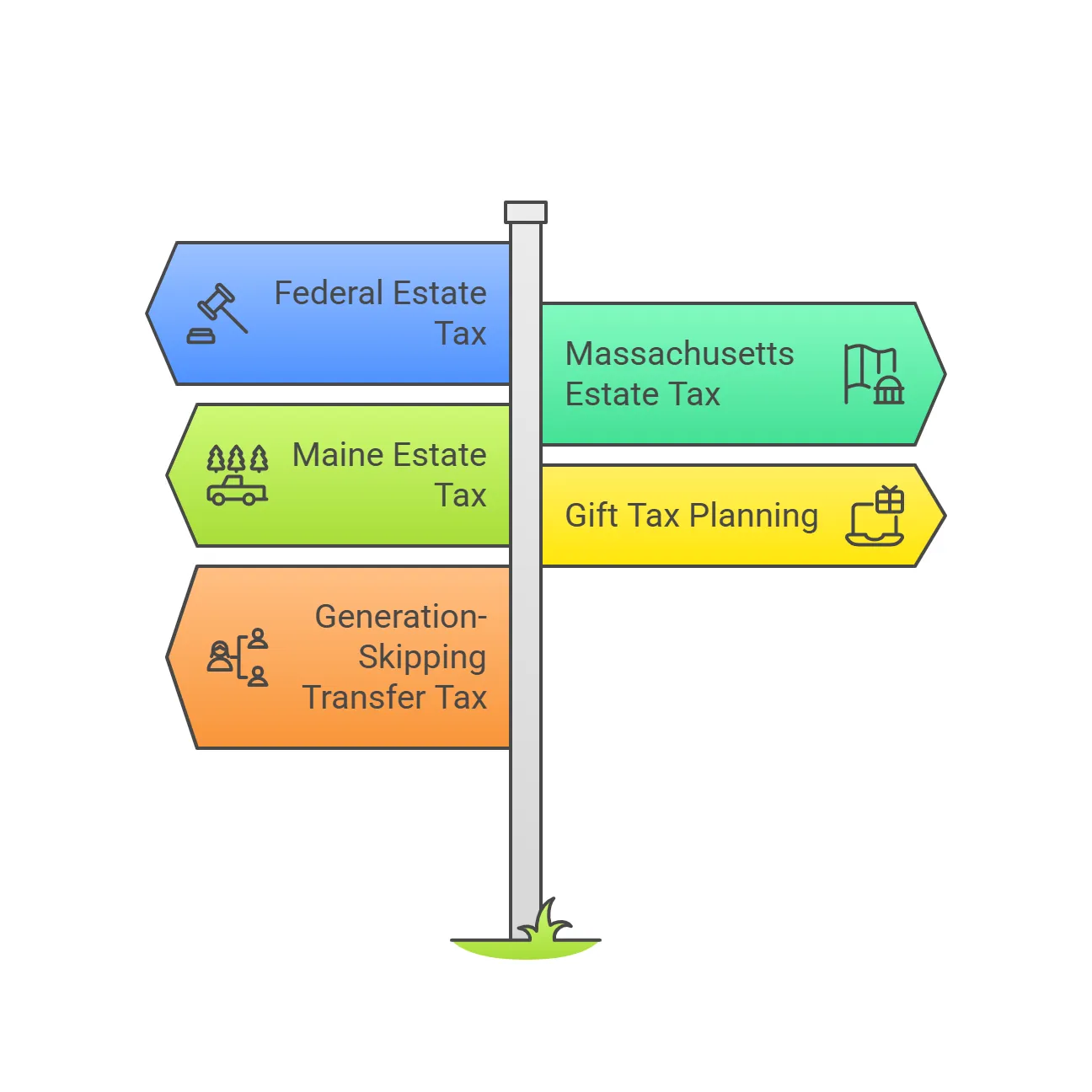

Tax Planning Strategies for Massachusetts & Maine Families

Smart planning protects more of what you’ve earned. For 2025, the federal estate tax basic exclusion is $13.99 million per person, and the annual gift tax exclusion is $19,000 per recipient.

Married couples can preserve portability (DSUE) for the survivor—but only by timely filing Form 706, even when no federal estate tax is due.

Massachusetts imposes an estate tax above $2,000,000 (not portable), while Maine excludes $7,000,000 per decedent, with 8%/10%/12% brackets above that amount.

We design plans that coordinate federal and state rules—without adding complexity to your family’s needs.

Federal Estate Tax

In 2025, the federal estate and gift tax exemption is $13.99 million per person. This means estates under that amount pass tax-free at the federal level. However, for high-value estates, tax rates can reach as high as 40%.

Early planning — through trusts, charitable giving, or strategic gifting — ensures more wealth stays with your heirs rather than being lost to taxation.

Massachusetts Estate Tax

Massachusetts applies one of the lowest thresholds in the nation: $2 million. Even families with moderate assets can face significant tax obligations.

A family home, retirement savings, and life insurance proceeds can quickly push estates above this limit.

Thoughtful planning strategies, including marital trusts and gifting, can help reduce or eliminate liability.

Maine Estate Tax

Maine is more generous, offering a $7 million exemption per person. Estates exceeding that amount are taxed progressively at rates ranging from 8% to 12%.

For families with businesses, real estate, or multi-generational assets, proper planning is essential to shield wealth from unnecessary taxation while maximizing the state’s favorable exemption.

Gift Tax Planning

The IRS allows individuals to give up to $19,000 per recipient in 2025 without touching their lifetime exemption.

Strategic gifting during your lifetime not only reduces the size of your taxable estate but also enables you to support loved ones immediately.

Larger gifts can be coordinated with your lifetime exemption for even greater tax efficiency.

Generation-Skipping Transfer Tax

The GST exemption mirrors the federal estate tax exemption at $13.99 million in 2025. Families often use dynasty trusts and other advanced strategies to transfer wealth directly to grandchildren or beyond.

This approach can avoid double taxation and preserve assets across multiple generations.

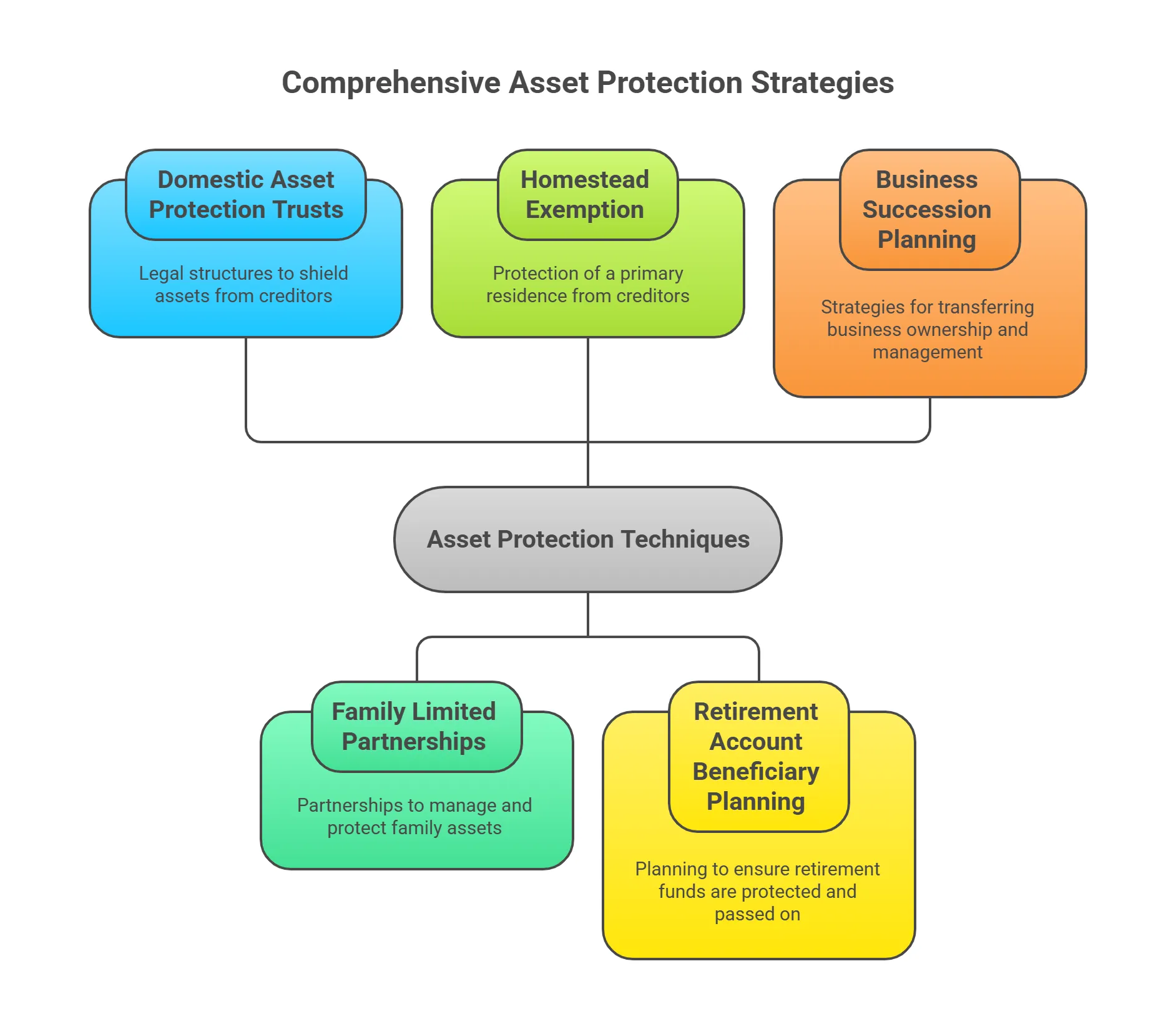

Asset Protection Techniques for Massachusetts & Maine Families

Preserving wealth is just as important as growing it. Estate planning isn’t only about distributing assets after death — it’s also about protecting what you’ve built during your lifetime.

With the right strategies, families can shield property, investments, and businesses from unnecessary taxes, creditors, and disputes.

In Massachusetts, a declared homestead can shield up to $1,000,000 of primary-residence equity (automatic protection remains $125,000).

Massachusetts and Maine are not DAPT states; when clients need a self-settled asset-protection trust, we coordinate out-of-state options and carefully address conflict-of-laws and creditor-rights limits.

When self-settled asset protection is appropriate, we evaluate out-of-state DAPT jurisdictions (e.g., NV/SD/DE) and address choice-of-law and creditor-rights limits for Massachusetts/Maine residents.

Family Limited Partnerships

A Family Limited Partnership (FLP) consolidates family assets — such as real estate, investments, or business interests — under one legal entity.

This structure reduces estate tax exposure, limits liability, and provides a controlled way to transfer wealth to future generations.

Homestead Exemptions

Homestead exemptions protect a portion of your primary residence from creditors.

- Massachusetts: Up to $500,000 of equity in a primary residence may be protected.

Massachusetts homestead: automatic $125,000, up to $1,000,000 with a Declaration;

MA vs ME

Topic | Massachusetts | Maine |

Estate tax threshold (2025) | $2,000,000 (no portability) | $7,000,000 (no portability) |

Homestead (creditor protection) | Up to $1,000,000 with declared; $125,000 automatic | |

Federal coordination | DSUE via Form 706 election | DSUE via Form 706 election |

Planning focus | Credit-shelter/marital trusts; Liquidity, situs, timing of bequests for brackets | Credit-shelter/marital trusts; Liquidity, situs, timing of bequests for brackets |

Retirement Account Beneficiary Planning

Retirement accounts are often among the largest assets a family owns. Choosing the right beneficiaries — and considering spousal rollovers or stretch provisions — ensures tax efficiency and protection. Poor planning can accelerate tax liability or expose accounts to unintended heirs.

Business Succession Planning

For families who own businesses, succession planning is vital. A clear plan determines who will manage or inherit the company, ensures continuity, and minimizes conflict. Tools like buy-sell agreements and trusts protect both the business and family harmony.

Special Considerations by State

Massachusetts

Massachusetts imposes an estate tax on estates exceeding $2 million. Even moderately sized estates may face tax liability.

Careful planning, including the use of trusts, gifting, and exemptions, is crucial to preserving family wealth.

Maine

Maine offers a $7 million estate tax exemption (2025), which shields most estates. Multi-State Issues

For families with ties to both Massachusetts and Maine, or property across state lines, establishing a proper domicile is crucial.

Multi-state property owners should consider domicile issues, as both property in Maine and Massachusetts may cause inheritance tax implications depending on property location and residency.

Courts and tax authorities closely examine where you legally “reside” when determining tax obligations and which state laws apply.

Life Events That Require Updating Your Estate Plan

An estate plan is not a “set it and forget it” document. Life changes quickly, and without regular updates, even the most carefully designed plan can become outdated or ineffective.

Experts recommend reviewing your plan every 3–5 years, and especially after major life events, such as those listed below.

Marriage, Divorce, or Remarriage

Marriage immediately changes legal and financial rights. Divorce or remarriage creates even greater complexity, especially with blended families.

Updating your estate plan ensures assets go to the right people, avoids accidental disinheritance, and protects children from prior relationships.

Birth or Adoption of Children

Welcoming a new child into your family is one of the most important reasons to update your plan. Parents should name legal guardians, create trusts to manage their inheritance responsibly, and ensure financial protection in the event of an unexpected occurrence.

Significant Asset Changes

Buying a new home, selling property, or receiving a large inheritance can shift your estate’s value dramatically.

Updating your plan ensures new assets are included and protected, while tax strategies remain optimized.

Moving Between States

Estate planning laws vary from state to state. A move from Massachusetts to Maine, or to another state entirely, may alter tax obligations, probate rules, or eligibility for certain exemptions. A review ensures compliance with your new state’s laws.

Business Ownership Changes

Starting, selling, or transferring a business can dramatically impact your estate plan.

Without proper updates, ownership disputes, succession issues, or tax burdens may threaten the company’s future. Planning ahead secures both your business and your legacy.

Domicile & Situs Checklist (MA ↔ ME movers)

You should update: driver’s license & vehicle registration, voter registration, resident state tax filings, mailing address with banks/insurers/advisors, Declarations of Domicile, any primary-residence filings, and refresh wills/trusts/POAs/health-care proxies for governing law and situs.

You should ensure you maintain consistent filings across the IRS, Massachusetts DOR, and Maine Revenue Services.

Secure peace of mind for yourself and your loved ones. Schedule your estate planning consultation with Spinnaker Probate Group now.